REAL ESTATE: LUXEMBOURG INVESTMENTS IN FRANCE

LUXEMBOURG REAL ESTATE INVESTMENT IN FRANCE HAS BECOME COMPLEX

The successive modifications (2017 & 2020) of the tax treaty between France and Luxembourg call into question the attractiveness of France.

This change of framework has not diminished the attractiveness of Luxembourg for European real estate investments.

From now on, the interest to invest in France is to be reviewed through 3 points:

- Anti-abuse clauses in the bilateral tax treaty which limit its advantages;

- Rescripts are more rarely granted by the Luxembourg administration;

- The French SCI as a new structuring scheme for real estate investment.

I. The SIF (Specialised Investment Fund)/OPCI (Undertaking for Collective Financial Investment) structuring is no longer relevant as the tax treaty has put an end to this practice when the Luxembourg shareholder holds at least 10% of the capital of the OPCI (Undertaking for Collective Financial Investment).

For more information:

II. The French SCI held by a Luxembourg company (SA, SARL, SAS...)

In this case the investor must now detach himself from the idea of a symbolic taxation in the current political and legal environment.

Taxation of property income and capital gains on the sale of assets will take place in France. The tax treaty which recognises the status of resident SCI also imposes a Luxembourg taxation which should normally be eliminated by the imputation on the Luxembourg tax of a tax credit equal to the French tax.

#real estate #investment #luxembourg #france #tax #taxation

Maître Saliha DEKHAR

ETUDE SD LAW - LUXEMBOURG

Other suggestions

-

REAL ESTATE: SPECULATION IS BACK FOR SUBLETTING!

-

Défauts, vices cachés automobile: les pièges à éviter

-

REAL ESTATE: DELAYS, MALFUNCTIONS, DEFECTS - YOUR RECOURSES

-

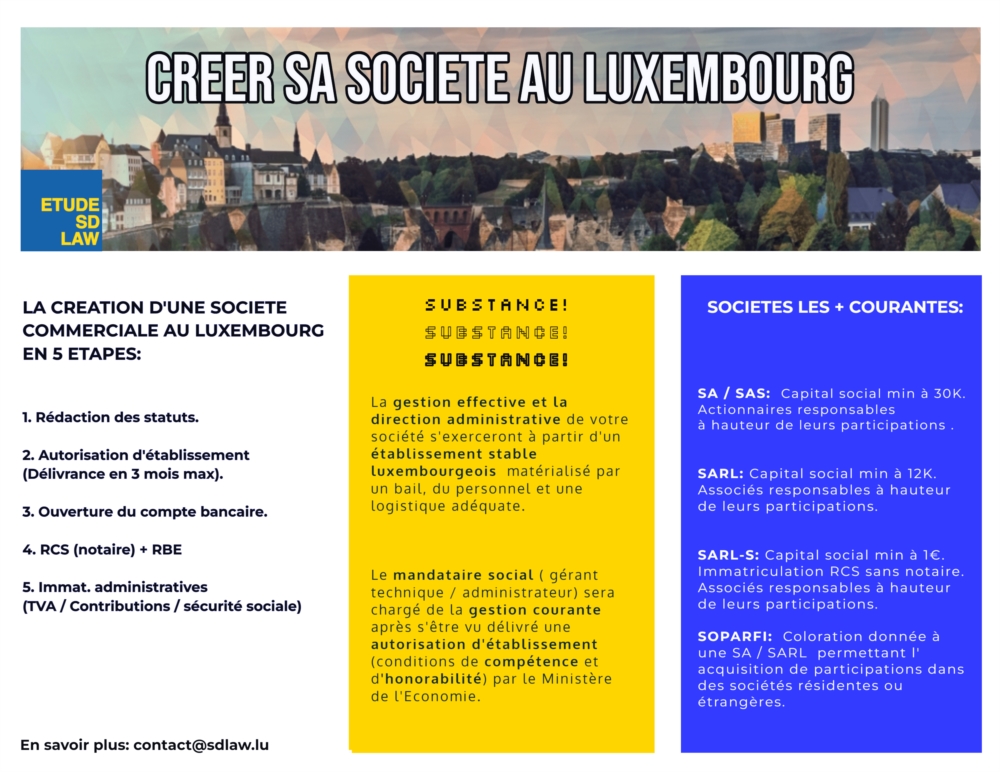

5 KEYS TO SETUP YOUR COMPANY IN LUXEMBOURG

-

LUXEMBOURG: UNFAIR COMPETITION, COMMERCIAL PARASITISM

-

AUTHORISATION TO OPEN A RETAIL ESTABLISHMENT